Adjusting Inventory

Although QuickBooks can automatically update your inventory when items are received and sold, you’ll need to manually adjust inventory to account for gains and shrinkage (theft, breakage, etc.):

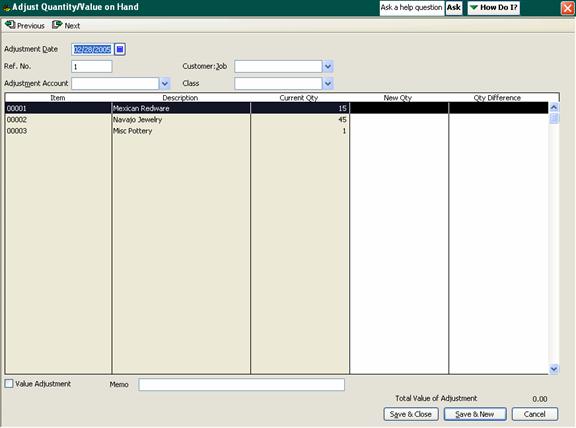

- From the Vendors menu, select Inventory Activities, and then select Adjust Quantity/Value on Hand from the submenu.

The Adjust Quantity/Value on Hand window opens.

- Confirm the date and enter a reference number (optional).

- Select the adjustment account from the drop-down menu. For losses, this will be an expense account associated with the loss; for gains, it will be an income account.

Note: You should create separate adjustments for each account.

- Select the associated customer and class, as appropriate. This is optional.

- To adjust the quantity of an item in the inventory list, enter the new quantity or the difference in quantity (whichever you prefer) into the appropriate column.

- To update the value of inventory items, select the Value Adjustment checkbox. This displays the New Value column. Enter the new value of the items you’re adjusting.

- Click Save & Close to update the inventory.